Superb Guidance To Assist You With Home Mortgages

Read the Full Report create by-Aggerholm LindahlOnce upon a time home mortgages were easy to get; lenders from all around the nation were eager to hand out some money. These days, however, easy mortgages have gone the way of the Dodo. In order to locate a great home mortgage loan that's easy to get and won't leave you paying insane interest, you may want to use some tips to guide you.

Don't put off a possible new mortgage any longer, or you're just wasting money. Chances are very good that with a new mortgage, you can pay a significantly lower amount of money every month. Look into all your options, shop around, and then decide on the terms that will suit your budget well, and save you the most cash!

Remember that the interest rate isn't the most important part of a mortgage. You also have to think about closing costs, points and other incidentals. There are different kinds of loan as well. That is why you have to find out as much as you can about what you're eligible for.

Make sure that all of your loans and other payments are up to date before you apply for a mortgage. Every delinquency you have is going to impact your credit score, so it is best to pay things off and have a solid payment history before you contact any lenders.

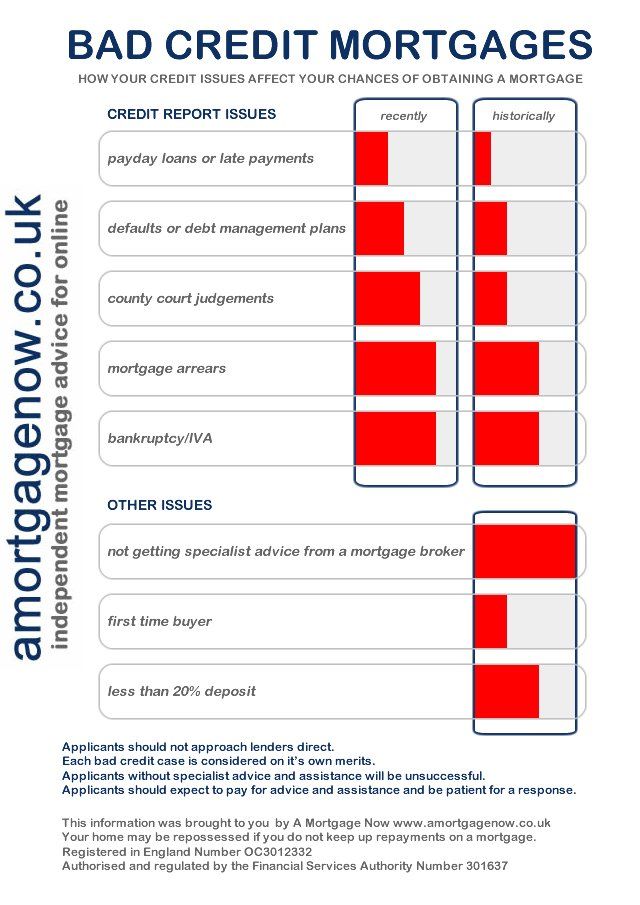

Find out how much your mortgage broker will be making off of the transaction. Many times mortgage broker commissions are negotiable just like real estate agent commissions are negotiable. Get this information and writing and take the time to look over the fee schedule to ensure the items listed are correct.

When you see a loan with a low rate, be sure that you know how much the fees are. Usually, the lower the interest rate, the higher the points. These are fees that you have to pay out-of-pocket when you close your loan. So, be aware of that so you will not be caught be surprise.

Try going with a short-term loan. Since interest rates have been around rock bottom lately, short-term loans tend to be more affordable for many borrowers. Anyone with a 30-year mortgage that has a 6% interest rate or higher could possibly refinance into a 15-year or 20-year loan while still keeping their the monthly payments near around what they're already paying. This is an option to consider even if you have slightly higher monthly payments. It can help you pay off the mortgage quicker.

Try going with a short-term loan. Since interest rates have been around rock bottom lately, short-term loans tend to be more affordable for many borrowers. Anyone with a 30-year mortgage that has a 6% interest rate or higher could possibly refinance into a 15-year or 20-year loan while still keeping their the monthly payments near around what they're already paying. This is an option to consider even if you have slightly higher monthly payments. It can help you pay off the mortgage quicker.

Really think about the amount of house that you can really afford. Banks will give you pre-approved home mortgages if you'd like, but there may be other considerations that the bank isn't thinking of. Do you have future education needs? Are there upcoming travel expenses? Consider https://azbigmedia.com/business/banking-industry/gainey-business-bank-earns-fdic-conditional-approval/ when looking at your total mortgage.

Pay your credit cards on time if you are considering a home mortgage in the next few years. Your credit score and debt to income ratios will come into play when you go for a home mortgage. If you have multiple late payments or are carrying a lot of debt, you may find the mortgage offers you receive to be poor.

If your mortgage has you struggling, seek assistance. Think about getting financial counseling if you are having problems making payments. Counseling agencies are available to you wherever you may live and many are sponsored by HUD. With the help of HUD-approved counselors, you can get free counseling for foreclosure-prevention. Look online or call HUD to find the nearest office.

You may be so excited about getting a new home that you go out and start buying all types of furniture. Unless you are paying for the furniture in cash, you need to hold off on this. You don't want to open any lines of credit or make any large purchases until after your loan is closed.

When shopping for a mortgage loan, ask if the rate is adjustable or fixed. Adjustable rate loans have interest rates which can vary greatly during the life of the mortgage. Also, your monthly payments will never be fixed and can increase by hundreds of dollars monthly. If the rate on the loan is adjustable, ask how and when the loan payment and rate could change.

After your mortgage is approved, continue to manage your credit responsibly. Your mortgage broker will check your credit again before finalizing the deal. If you decide to go out and charge a trip to Tahiti on your credit card to celebrate your new home, you could very well lose your home mortgage! Simply sit tight and continue making timely payments on the debts you have until you are firmly situated in your new home.

Ask the seller to take back a second if you are short on your down payment. Since the market is slow right now, a seller might be willing to step in and help. You will end up making two payments each month, but this will enable you to get a mortgage.

If you have a little bit more money to put down on a home, consider getting a conventional mortgage as opposed to an FHA mortgage. FHA mortgages have lower down payments, but excessive fees that are added to the cost of the mortgage. Save up at least 5 percent in order to be eligible for an FHA loan.

Prior to meeting with a mortgage broker, decide what your budget is. If it should be that a lender gives you more money than you can pay back monthly, you'll have some extra room. Just be careful not to bite off more than you can chew. Doing this may make you have a lot of problems with finances later on.

Don't be fooled by mortgage lenders that say there are "zero costs" to you at closing. It's typically a marketing ploy. The mortgage company places those funds either into the loan itself, or they are charging you a higher interest rate for the zero cost privilege. Either way, know that you are paying more over time.

As you can see, there's a lot you don't know about the home mortgage business. Using tips like the ones listed above can help you to not only locate a loan but they can also ensure that you find a low-interest loan that won't leave you playing catch-up on a month-to-month basis. So always seek out information before acting.